Silicon Hegemony: Unraveling the AI Infrastructure Supercycle

VeloTechna Editorial

Observed on Jan 15, 2026

Technical Analysis Visualization

VELOTECHNA, Silicon Valley - In the current era of digital transformation, the architecture of global trade is being rewritten not in code, but in silicon. The global technology landscape is currently undergoing a major shift, transitioning from general-purpose computing to an era defined by accelerated processing and generative intelligence. This transition is not just an incremental upgrade but a total reconfiguration of the global supply chain, as highlighted in recent industry reports on the dominance of high-performance computing modules and the strategic maneuvering of semiconductor giants. According to source recently, the concentration of power in the AI hardware sector has reached a critical threshold, forcing hyperscale countries and sovereign states to rethink their long-term digital sovereignty.

Hardware Bottleneck Mechanisms

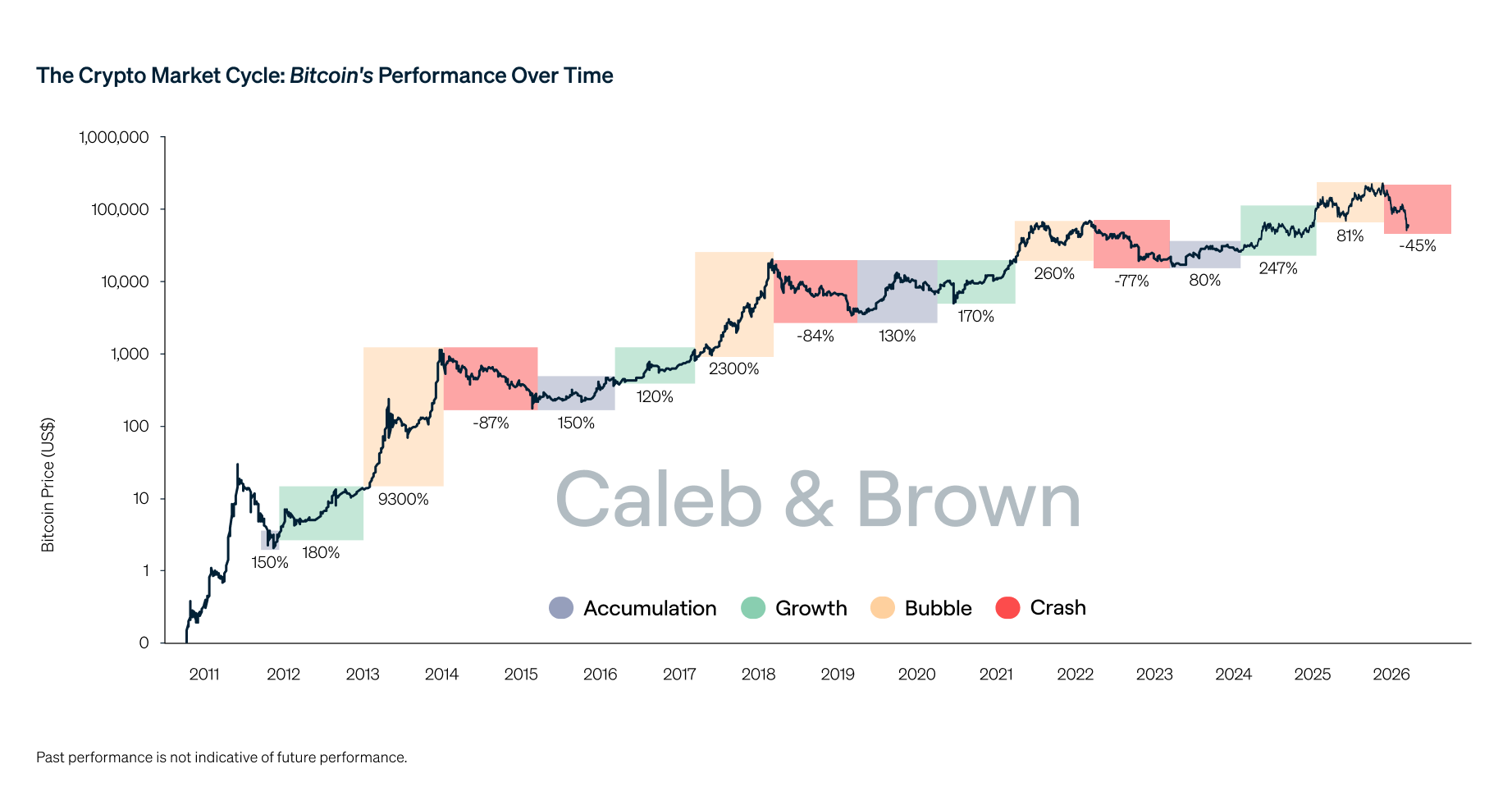

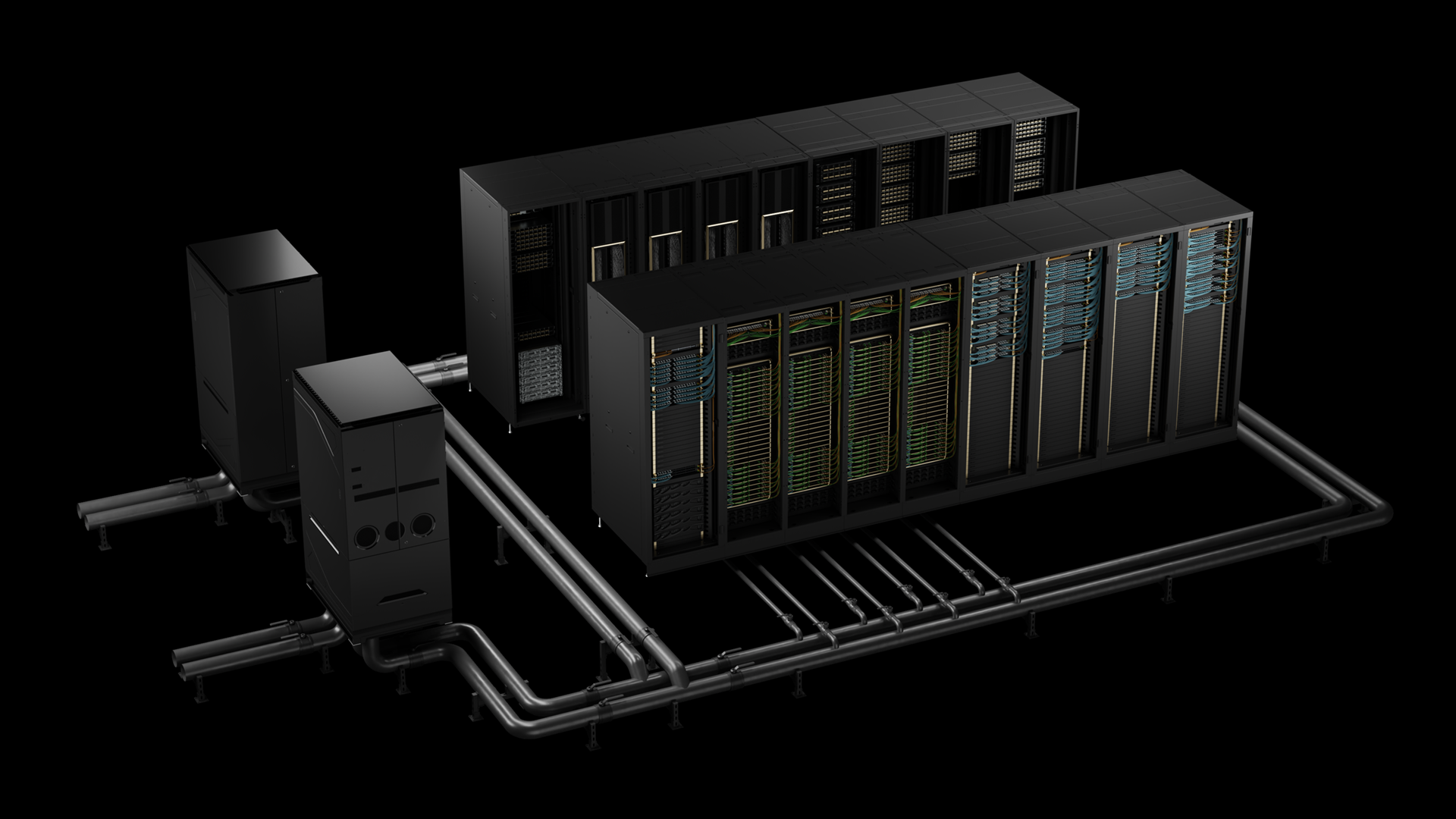

The technical mechanisms driving this supercycle are rooted in the specific requirements of the Large Language Model (LLM). In contrast to traditional CPU-centric architectures that handle sequential tasks, the AI era demands parallel processing capabilities that only high-end GPUs and dedicated ASICs (Application Specific Integrated Circuits) can provide. VELOTECHNA analysts have observed that the scarcity of High Bandwidth Memory (HBM3) and CoWoS (Chip-on-Wafer-on-Substrate) packaging capacity has created bottlenecks that go beyond simple manufacturing processes. It's a logistical deadlock where demand currently exceeds supply by a factor of nearly three to one. These mechanical constraints have turned silicon into 'digital gold', where the ability to secure a procurement roadmap is as valuable as the intellectual property software being developed.

Main Players and Custom Silicon Search

While NVIDIA remains the undisputed industry giant, controlling the vast majority of data centers GPU market, the competitive landscape is increasingly diverse. The main players are no longer just chip designers like AMD and Intel, but also large-scale consumers themselves. Google, Amazon, and Microsoft are aggressively turning to custom silicon—TPU, Trainium, and Maia—to reduce their dependence on external vendors and optimize their specific workloads. This 'insourcing' of hardware design represents a fundamental shift in the technology ecosystem. By controlling the stack from the transistor level to the API, these giants build moats that make it increasingly difficult for smaller startups to bridge, creating a divided market of 'compute haves' and 'compute have-nots.'

Market Reaction and Capital Realignment

The market reaction to this change has been extraordinary. We have witnessed a massive reallocation of capital from software-as-a-service (SaaS) ventures towards infrastructure investments. Institutional investors are no longer satisfied with high margins alone; they examine the 'computing resilience' of companies. Valuations of companies that have secure access to Blackwell-class chips or proprietary fabrication agreements have skyrocketed, while companies that rely on legacy cloud infrastructure have seen their multiples decline. This alignment suggests that the market now views AI hardware not as a commodity expenditure, but as a strategic asset comparable to the oil reserves of the 20th century.

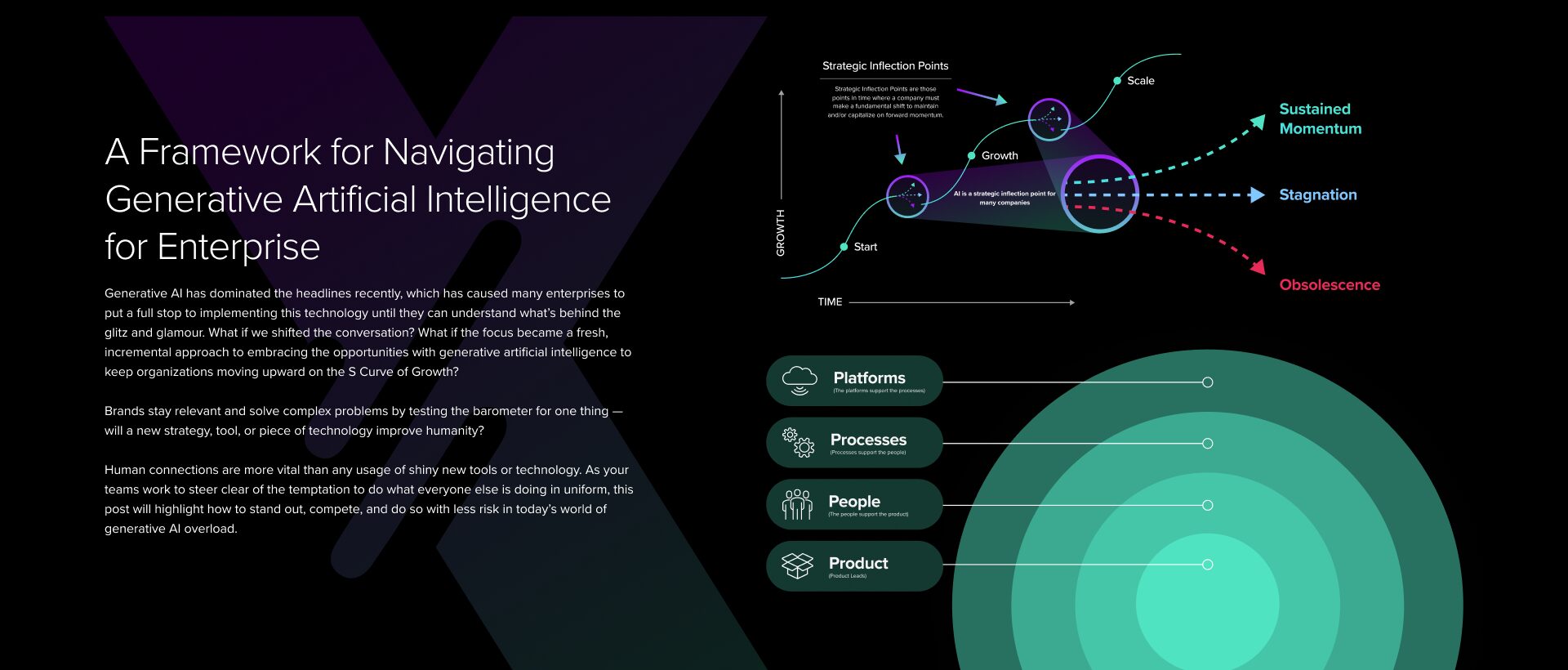

Impact and Two-Year Analytical Forecast

Looking ahead, VELOTECHNA expects a two-phase evolution over the next 24 months. In the first year, we expect 'Normalization of Scarcity'. As new fabrication facilities come online and packaging techniques improve, extreme supply shortages will begin to lessen. However, this will not lead to a reduction in prices; instead, this will lead to a surge in adoption of 'Edge AI'. We expect the focus will shift from large centralized training clusters to localized, high-efficiency inference hardware integrated directly into consumer devices and industrial IoT nodes.

At the end of the second year, the industry will likely face an 'Efficiency Reckoning'. As the initial hype around generative models matures, the focus will shift from raw power to performance per watt. The winners of this phase will be those who can provide sustainable and energy-efficient computing solutions. We anticipate that the total AI-optimized silicon market will grow by 35% by 2026, driven largely by the integration of AI into traditional manufacturing and healthcare sectors, where it is currently still in the pilot phase of implementation.

Conclusion

Silicon hegemony is more than just a corporate race; this is the foundation of the next industrial revolution. As computing power becomes a key driver of economic productivity, the strategic importance of the semiconductor supply chain will only increase. For leaders and investors, the message is clear: in the age of intelligence, hardware is the strategy. Those who fail to secure their place in the silicon hierarchy risk being considered outdated by the algorithms they seek to implement. VELOTECHNA will continue to monitor these developments as the boundaries between physical hardware and cognitive software continue to disappear.

Sponsored

Lanjutkan dengan Word Counter

Ukur kepadatan konten analisis dan reading time.